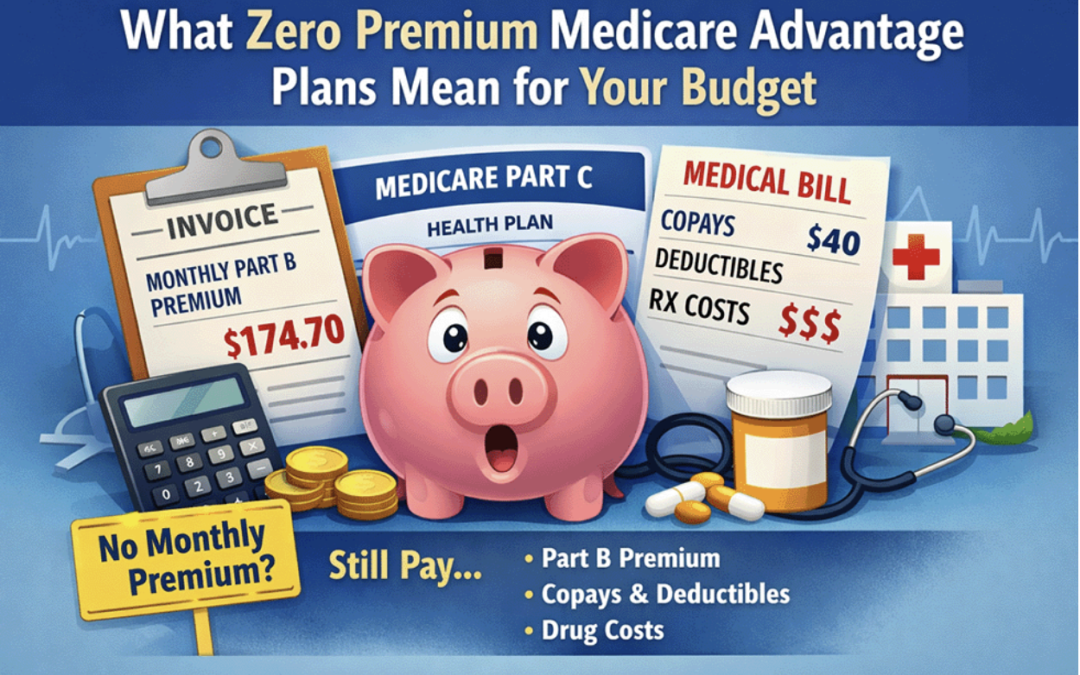

Zero premium Medicare Advantage plans sound like a great deal… until you get the bill.

A $0 premium means you don’t pay a monthly fee to the private insurer offering the plan, but it doesn’t mean your healthcare is free. You still have to pay the standard Medicare Part B premium and cover other costs like copays, coinsurance, and deductibles.

For many people, these expenses add up quickly, especially when specialist visits or hospital care are involved.

For many people, these expenses add up quickly, especially when specialist visits or hospital care are involved.

According to KFF, the average Medicare Advantage enrollee paid about $4,972 out-of-pocket in 2022, not including the Part B premium. While zero premium plans lower the monthly bill, they can still lead to thousands in annual costs depending on how often you use healthcare services.

At Absolute Best Insurance, we help people across Florida choose Medicare Advantage plans that actually match their healthcare needs and financial goals. We take the time to explain what zero premium really means for your budget, and we’ll even come to your home if that’s easier for you.

What Does “Zero Premium” Really Mean?

A zero premium Medicare Advantage plan means you don’t pay a monthly premium to the private insurer that administers the plan. But you still have to pay your Medicare Part B premium, which will cost $202.90 per month in 2026, according to Medicare.gov.

These plans are part of Medicare Part C, also known as Medicare Advantage. They’re funded in part by the government, so some insurance companies can offer $0 premium plans in competitive markets.

Zero premium doesn’t mean zero cost. Most plans include copays, deductibles, or coinsurance when you get care. You may also pay the full cost for out-of-network services or higher-tier medications.

What’s Covered in a $0 Premium Plan?

Medicare Advantage Part C plans typically include:

- Primary care and specialist visits

- Preventive services like screenings and vaccines

- Prescription drug coverage

- Telehealth

- Some dental, vision, and hearing benefits

- Over-the-counter benefits and gym memberships

Coverage varies by ZIP code and insurer. Some plans focus more on chronic condition management, others on fitness or transportation. You’ll need to compare plans based on your specific health needs and local provider network.

What Out-of-Pocket Costs Should You Expect?

Even with zero premium plans, out-of-pocket costs can add up. Most plans charge:

- Copays for office visits, urgent care, and prescriptions

- Coinsurance for hospital stays or surgeries

- Deductibles for certain services

- Out-of-network penalties if you see a provider outside your plan

The federal Maximum Out-of-Pocket for in-network care under Medicare Advantage is $9,250. After you hit this maximum, your plan pays 100 percent of covered services for the rest of the year.

When a $0 Premium Plan Makes Sense

Zero premium Medicare Part C plans can make sense if:

- You rarely visit the doctor

- You don’t take many prescriptions

- Your preferred providers are in-network

- You need low monthly costs over all-inclusive benefits

They’re also attractive for veterans who use VA benefits for major care, or for people with limited income who qualify for Extra Help or Medicaid.

When It Might Not Be a Good Fit

A $0 premium Medicare Advantage plan may cost more long-term if:

- You have chronic conditions that require regular specialist visits

- Your medications fall into higher cost tiers

- You want to see out-of-network providers

- You need coverage for major surgeries or inpatient stays

Some people prefer the predictability of higher premium plans with lower out-of-pocket costs and broader networks.

Medicare Part C vs Medigap: Cost Considerations

It’s worth comparing Part C plans with Medigap policies. While Medigap has higher monthly premiums, it typically covers more out-of-pocket costs. Part C plans offer extra benefits but come with network restrictions and variable costs.

If you prefer simplicity and a capped out-of-pocket limit, Part C may work.

If you want flexibility and minimal billing surprises, Medigap plus Part D might be better.

Budgeting Tips for Choosing a Plan

Don’t choose a plan based on the premium alone. Here’s what else to review:

- Check the total maximum out-of-pocket limit

- Review the copay chart for your common services

- Look up your prescriptions in the drug formulary

- Make sure your doctors and hospitals are in-network

- Compare emergency and urgent care coverage

We help clients build a real healthcare budget, not just compare plan flyers. We’ll run the numbers with you.

We Help You Understand What You’re Really Paying For

Zero premium plans can work, but they’re not the cheapest in every case. It all depends on your usage, network preferences, and prescriptions. That’s where we come in.

We’ve helped hundreds of Florida residents across cities like Tamarac, Greenacres, Port St. Lucie, and Vero Beach find the right plan. We explain it all clearly, offer comparisons, and even make house calls.

| “A $0 premium plan might look like a deal, but what matters is what you’ll pay when you actually use the plan.” – Stacy Murphy, Owner of Absolute Best Insurance |

Ready to Compare Real Costs?

If you’re looking at zero premium Medicare Part C plans, we’ll help you break down the numbers before you make a decision. Our team can answer your questions, show you plan options available in your ZIP code, and walk you through every benefit.

Get started today. Your budget deserves the right coverage.

Visit one of our Absolute Best Insurance offices in Tamarac, Deerfield Beach, Greenacres, Port St. Lucie, Micco, or Vero Beach to review your coverage options.

Click here or give our team a call for a free, no-obligation quote. We even make house calls!

- Tamarac: (954) 642-2101

- Deerfield Beach: (754) 778-8700

- Greenacres & Vero Beach: (561) 420-0280

- Port St. Lucie: (772) 828-2840

- Sebastian (Micco): (772) 321-0813